![]()

Islamic Banking and Finance. Riba

WhatsApp

WhatsAppIslamic financial system (two prohibitions) Riba and speculation

The Islamic financial system (based on Sharia) prohibits riba (usury or interest), gharar (excessive uncertainty), and investments in haram (forbidden) activities, such as alcohol or gambling. This gave rise to financial instruments such as mudarabah (partnership of capital and labor) and sukuk (Islamic bonds). Zakat (obligatory charity) encourages wealth redistribution.

An Islamic Bank cannot be a single lender who is not involved in business, the Islamic Bank should take a more active role, should be a financial partner, the Islamic Bank assumes the risks of the company and therefore have a part of business ownership.

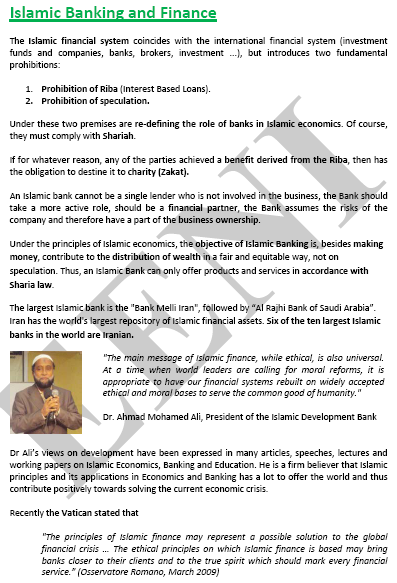

“When the leaders of the World are searching for financial reforms; it is desirable to have a global financial system built on ethical and moral foundations widely accepted for the common good of humanity.” PhD Ahmad Mohamed Ali, President of the Islamic Development Bank

- Introduction to the Islamic Banking and Finance System

- Fundamental Prohibitions: Speculation and Interest Based Loans

- Compliance with the Sharia for financial products and services

- Types of loans in the Islamic Banking: Al-Mudaraba, Al-Murabaha, and Al-Musharaka

- Islamic Banks in the World

- Religion and ethical frameworks

- Influence of religion on financial systems

- Cases of banks and bankers applying the principles of Islamic Banking

- Islamic Development Bank

- Mohammad Abdul Mannan

- Sulaiman Al-Rajhi

- Jawad Ahmed Bukhamseen

Sample - Islamic Banking and Finance (Islamic Civilization)

Religions and Global Business -

Religious diversity

The Subject “Islamic Banking” is included within the curriculum of the following academic programs at EENI Global Business School:

Master: Religions & International Business, Business in Africa, International Business.

Doctorate: Ethics, Religions & Business, World Trade.

Languages:  or

or  Banca Islámica

Banca Islámica  Banque islamique

Banque islamique  Banca Islâmica.

Banca Islâmica.

Islamic Banking and Finance.

The Islamic financial system coincides with the international financial system (investment funds and enterprises, banks, brokers, and investment), but introduces two fundamental prohibitions:

- Prohibition of Riba (Interest Based Loans)

- Prohibition of Speculation

Under these two premises are re-defining the banks role in the Islamic Economics. Of course; an Islamic Bank must comply with Sharia.

Recently the Vatican stated that:

“The principles of Islamic Finance may represent a possible solution to the global financial crisis.” (Osservatore Romano, March 2009).

Under the Islamic Banking system there are mainly three types of loans:

- Al-Mudaraba

- Al-Murabaha

- Al-Musharaka

If for whatever reason, any of the parties achieved a benefit derived from Riba then has an obligation to destine it to charity (Zakat).

Under the principles of Islamic Economics, the objective of the Islamic Banking is, besides making money, contribute to wealth distribution in a fair and equitable way, not on speculation. Thus, an Islamic Bank can only offer products and services in accordance with Sharia law.

The largest Islamic Bank is the “Bank Melli Iran,” followed by the “Al-Rajhi Bank of Saudi Arabia.”

- Iran has the world's largest repository of Islamic financial asset

- Six of the ten largest Islamic banks in the World are Iranian

Islamic banks, such as Dubai Islamic Bank, operate interest-free and use risk- and reward-sharing contracts. In 2023, the global Islamic finance market exceeded $4 trillion, according to the Islamic Finance Development Report.

The International Bank of Kuwait offers services of Islamic Banking.

Related information:

(c) EENI Global Business School (1995-2025)

Top of this page